If your car is totaled in Florida, your insurance will pay it off, but it can depend on our coverage. Standard auto insurance covers the car’s actual cash value (ACV), not what you owe on the loan. If you owe more than the car’s ACV, insurance is responsible for the difference—unless you have gap insurance, which covers the shortfall.

At Mubarak, Sherif & Oladipo (MSO), we guide clients through this complicated process. With unique insight from former insurance defense lawyers, we understand the ins and outs of these situations. We make sure our clients get personalized representation, not just any representation.

Key Takeaways

- Insurance payouts cover the actual cash value (ACV) of a totaled car, not necessarily the outstanding loan balance.

- The remaining loan balance after an insurance payout is the owner’s responsibility unless gap insurance is in place.

- Gap insurance covers the difference between the insurance payout and the loan balance only when the car is declared a total loss.

- Regular loan payments must be maintained after a total loss to avoid damaging credit scores, even if the insurance payout does not cover the entire loan.

What if My Car Is Totaled in an Accident in Florida?

If your car is totaled in Florida, you can accept the insurance payout or keep the vehicle, though keeping it may reduce the payout. If you still owe money, insurance must be maintained unless gap insurance covers the balance.

Florida law allows four years to file a car accident claim. Consulting a lawyer can help you understand the process and maximize your compensation.

What Does Totaled Mean?

A car is considered totaled when repair costs exceed its actual cash value (ACV), which insurers determine based on depreciation, mileage, and market conditions. Florida law mandates that totaled vehicles be reported for a salvage title through the Florida Department of Highway Safety and Motor Vehicles.

Can I Keep My Totaled Car?

Yes, you can keep your totaled car in Florida. After the insurance company pays the actual cash value (ACV), you can buy it back at its salvage value. However, you must obtain a salvage title and pass inspections before making it roadworthy again, which is regulated by the Florida Department of Highway Safety and Motor Vehicles.

Keeping a totaled car can lead to higher insurance costs. While specific premium increases vary, insurers may charge 20-40% more or restrict coverage to liability-only policies.

Will I Still Have to Pay Insurance on a Total Loss Car?

If your car is totaled, you may still need insurance, depending on your situation. If you have an outstanding loan, your lender typically requires you to maintain coverage until the loan is fully paid.

The insurance company will pay the car’s actual cash value (ACV) to the lender, but if the payout is less than the remaining balance, you are responsible for the difference unless you have gap insurance.

However, once the car is declared a total loss and ownership transfers, you can cancel your policy if there’s no outstanding loan. Always review your insurance policy for specific post-total-loss requirements.

How Does Insurance Determine If a Car Is Totaled?

Insurance companies determine if a car is totaled by comparing its repair costs to its actual cash value (ACV) before the accident. If repairs exceed a set percentage of the ACV—typically 70-80%, depending on state laws and insurer policies—the car is declared a total loss.

Florida, for example, uses an 80% total loss threshold. Some states apply a Total Loss Formula (TLF), where insurers add the salvage value to repair costs; if the sum exceeds the ACV, the car is totaled.

Insurers use valuation tools like Kelley Blue Book, NADA, and CCC One to determine ACV. Once totaled, they pay the car’s ACV, usually minus the deductible.

What is Actual Cash Value (ACV)?

Actual Cash Value (ACV) represents a vehicle’s pre-loss market value, which insurers use to determine payouts in total loss claims. It accounts for depreciation, mileage, condition, and market factors.

According to Edmunds, new cars lose about 19% of their value in the first year . Depreciation also makes up a portion of ownership costs.

The Role of Gap Insurance in Total Loss Situations

Gap insurance covers the difference if your car loan balance exceeds the insurance payout after a total loss.

When Does Gap Insurance Not Pay Out?

Gap insurance only covers the difference between your car’s actual cash value (ACV) and the remaining loan balance if the car is totaled or stolen. If the car isn’t officially totaled, gap insurance won’t apply. It does not cover:

- Repairs – Only total loss situations apply.

- Medical Bills – Covers the loan gap, not personal injury.

- Rental Cars – Separate coverage is required.

- Damage to Others’ Property – Liability insurance handles this.

What if I Still Owe Money For The Totaled Car?

If your car is totaled while you still have a loan, your financial responsibility depends on insurance coverage and liability. If you have collision or comprehensive insurance, the insurer pays the Actual Cash Value (ACV) of the car.

If the ACV is less than your loan balance, you must cover the difference unless you have gap insurance, which pays off the remaining loan amount. If another insured driver is at fault, their liability insurance should cover your car’s ACV, but if their policy limits are too low, your underinsured motorist coverage may help.

If you lack insurance, you must pay the remaining loan balance out of pocket, as the lender still requires payments even if the car is undrivable. Gap insurance is the best way to avoid unexpected financial burdens in a total loss situation.

What Happens to My Loan If the Other Driver Is At Fault for the Accident?

If the other driver is at fault, their insurance pays the Actual Cash Value (ACV) of your car. If the ACV is less than your loan balance, you must cover the difference unless you have gap insurance.

What Happens to My Loan If I Have Insurance?

If your car is declared a total loss, your insurance company’s payout may not fully cover your outstanding loan balance. You’ll be on the hook for the remaining amount unless you have gap insurance, which pays the difference between what’s owed on your car and its actual cash value.

What Happens When Insurance Does Not Cover the Entire Balance?

If your insurance payout is less than your loan balance, you must pay the difference. Gap insurance covers this shortfall.

Without gap coverage, you must negotiate a payment plan with your lender. The Consumer Financial Protection Bureau warns that failing to cover the gap can lead to financial strain. To avoid this risk, consider adequate insurance if you have an outstanding loan.

What Happens to My Loan If I Am At Fault and I Don’t Have Insurance?

If you are at fault in an accident without insurance, you are fully responsible for damages, injuries, and any remaining car loan balance. Without insurance, you must negotiate directly with your lender, increasing financial risk.

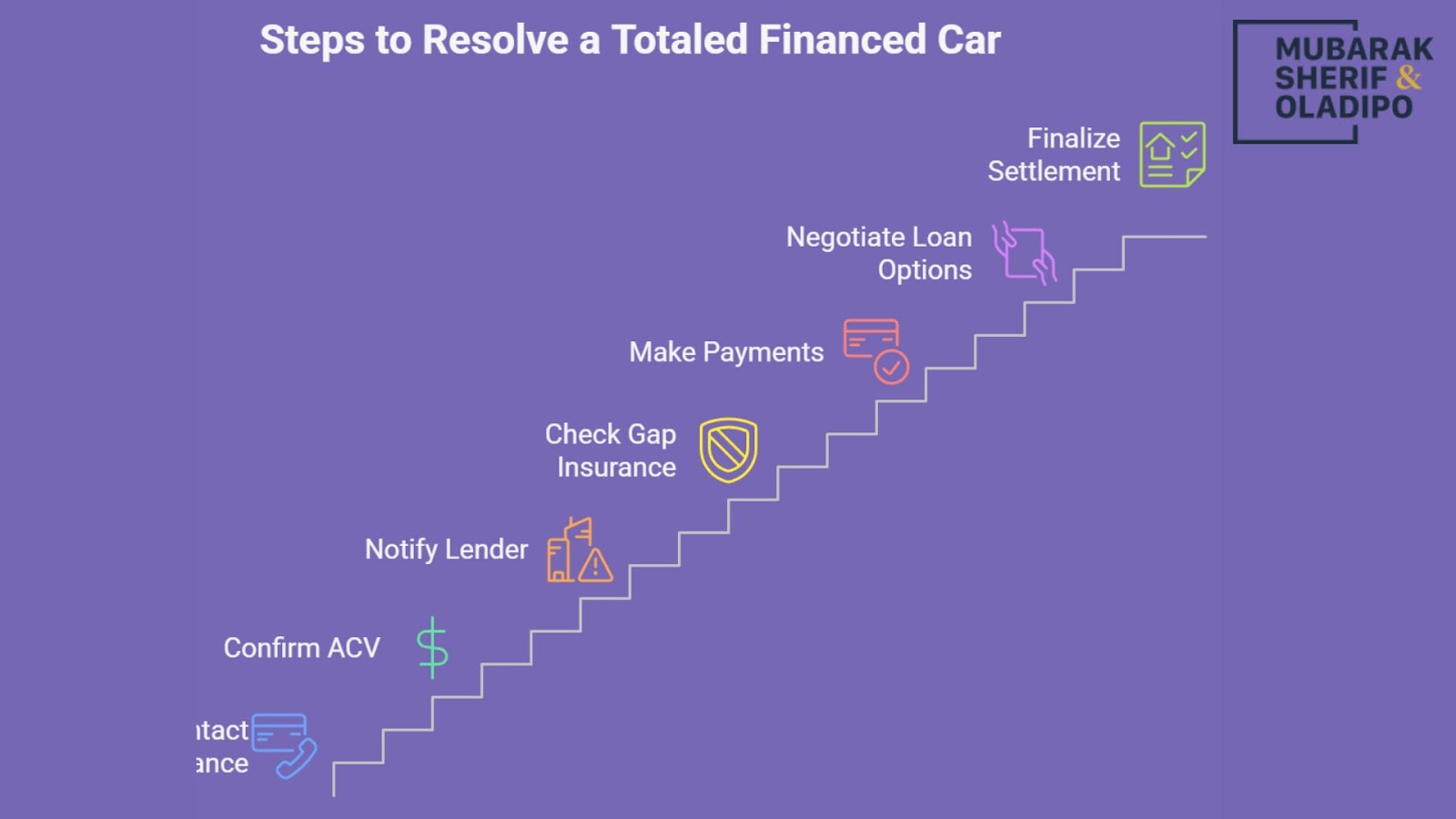

Steps to Take if Your Car Is Totaled and You Still Owe Money

Here are the steps to take if you have totaled your car and still owe money:

- Contact Your Insurance Company – Confirm the ACV payout and check if it covers your loan balance.

- Notify Your Lender – Your lender still expects payments until the loan is fully settled.

- Check for Gap Insurance – If you have it, it covers the remaining loan balance after the insurance payout.

- Continue Loan Payments – Missing payments hurts credit scores, and borrowers who stop paying can see score drops.

- Negotiate with Your Lender – If you can’t pay the difference, ask about loan settlement options or refinancing.

Why You Should Consult With a Lawyer

If your insurance payout doesn’t cover your loan, here’s how a lawyer can protect your financial interests.

- Insurance Claims Assistance: Lawyers make sure you get fair settlements.

- Understanding Coverage: Many drivers don’t fully understand their policies. Lawyers can assist with simplifying this process.

- Negotiation with Insurers: Insurers work to minimize payouts. A lawyer fights for fair compensation.

- Evidence Collection: Strong documentation improves claim outcomes. Lawyers help gather proof of your car’s condition and losses.

- Legal Guidance: A lawyer helps explore settlement options, lawsuits, and policy disputes.

Legal assistance increases your chances of a better payout and protects your financial future.

Get the Support You Need

Dealing with a totaled car and an unpaid loan can be overwhelming, but you don’t have to face it alone. Our team is here to help you handle insurance claims, lender negotiations, and legal options to protect your finances. Get the answers and support you need. Contact us today!