Being involved in a car accident can be stressful, but the situation becomes even more complicated if you’re found at fault. In Florida, protecting your assets after an at-fault accident requires understanding state laws, insurance coverage, and legal strategies to limit financial risk.

In most cases, your primary residence is protected under Florida’s Homestead Exemption, which prevents creditors from seizing your home.

However, this protection does not extend to all assets, meaning rental properties, savings, and other valuables could be at risk if the financial liability from an accident exceeds your insurance coverage.

Mubarak, Sherif & Oladipo brings a strategic edge to asset protection and personal injury law. With a team of former insurance defense lawyers, we understand the tactics insurance companies use and leverage this experience to protect your assets.

We have successfully handled 1,000 cases in just five years, securing over $50 million in recoveries. Our commitment to personalized legal representation makes sure that each client receives direct guidance from experienced trial lawyers, not case managers.

Key Takeaways

- Utilize Florida’s Homestead Exemption to protect your primary residence from potential seizures due to debt satisfaction.

- Maintain comprehensive insurance coverage, including bodily injury liability, to limit financial risks associated with at-fault accidents.

- Consult with legal professionals to develop asset protection strategies, especially if your liabilities exceed your insurance coverage.

- Keep your Personal Injury Protection (PIP) insurance current to secure immediate coverage of medical expenses and lost wages.

- Be aware of your personal insurance limits and explore additional coverage options to better protect yourself from potential lawsuits.

Can You Lose Your House Due to an At-Fault Car Accident in Florida?

Lawyer Reveals Easy Car Accident Claim Process

You can lose your home due to an at-fault car accident, but only under certain conditions. Florida’s Homestead Exemption protects homeowner financial security by protecting a primary residence from creditors.

However, according to the Florida Department of Highway Safety and Motor Vehicles, there were over 400,000 car accidents in Florida in 2022. If the liability from such an accident exceeds insurance coverage limits, other assets like rental properties might be endangered.

The Insurance Information Institute reports that in 2018, one-fourth of Florida motorists were uninsured, increasing the risk for losses beyond their insurance coverage. Adequate insurance coverage, particularly bodily injury liability, can significantly decrease financial vulnerability.

Legal advice options offer asset protection strategies, guiding homeowners through liability and compensation laws. Understanding these provisions allows one to preserve one’s home and offers peace of mind during the aftermath of an at-fault car accident.

What Is the Homestead Exemption?

The Homestead Exemption is a Florida law that protects a homeowner’s primary residence from being seized to satisfy most debts. According to the Hillsborough County Appraiser, Florida law allows up to $50,000 to be deducted from the assessed value of a primary/permanent residence. The first $25,000 of value is entirely exempt. T

What Properties Does Homestead Exemption Protect?

The Homestead Exemption applies to:

- A homeowner’s primary residence, regardless of value

- In 2022, 65.8% of Americans own homes (U.S. Census Bureau), making this exemption highly impactful.

- Urban properties within municipalities (up to half an acre)

- Urban areas make up just 3.6% of U.S. land (U.S. Department of Agriculture), making this provision crucial for city homeowners.

- Non-urban properties up to 160 acres

- In 2023 there were almost 900 million acres of farmland in the U.S. (National Agricultural Statistics Service), allowing rural homeowners to benefit significantly.

Additionally, some financial assets—such as wages and retirement accounts—may also be protected under certain conditions.

What Properties Are Not Protected by the Homestead Exemption?

Here are the property types that are not covered under the exemption:

- Rental and Commercial Properties

- Florida has a large market for rental and commercial properties, which are not shielded by the exemption, leaving investment real estate exposed.

- Abandoned Homestead Properties

- If a homeowner abandons a previously designated homestead, it loses exemption status.

- Properties Owned by a Business Entity

- The Homestead Exemption does not apply to properties held under LLCs or corporations. This could present a significant risk for business owners.

How Insurance Affects Your Risk

According to R Street Institute in 2023, Florida tops lists with more than 20 percent of drivers uninsured, compared to the national average of about 12 percent, leaving a large portion of the population vulnerable.

Attaining adequate coverage allows you to protect your home, savings, and other assets after an at-fault accident.

What Is Florida’s No-Fault Insurance Law?

Florida’s no-fault insurance law requires drivers to carry Personal Injury Protection (PIP) insurance, which covers medical expenses regardless of fault. This law helps drivers attain immediate medical coverage without waiting for liability disputes.

What Is Personal Injury Protection (PIP) Insurance in Florida?

Personal Injury Protection (PIP) insurance is mandatory in Florida and covers up to 80% of medical expenses and lost wages, regardless of fault. As a no-fault state, Florida requires all drivers to carry PIP for immediate financial support for treatment.

However, PIP has coverage limits and expiration rules that may leave gaps in protection. Understanding these limitations is important to protecting personal assets after an at-fault accident. A skilled injury lawyer can assist with understanding these limits.

Florida’s no-fault system simplifies medical claims but does not eliminate liability risks, making comprehensive coverage essential for financial protection after an at-fault accident

Bodily Injury Liability Risks in Florida

Bodily injury insurance is a type of liability coverage that helps pay for medical expenses, lost wages, and legal fees if you’re responsible for injuring someone in an accident. It’s typically part of an auto insurance policy and covers the other party’s costs—not your own.

Without bodily injury liability (BIL) coverage, victims may sue you for damages, putting your personal assets, including your home, at risk.

What to Do After an At-fault Accident?

Here are the steps you should take if you’re at fault in an accident in Florida:

- Assess Insurance Coverage: If damages exceed your coverage, your personal assets may be at risk.

- Seek Legal Counsel: A lawyer can help understand liability risks and protect your assets.

- Review & Enhance Insurance Coverage: Comprehensive insurance, including umbrella policies, can provide extra protection and help to manage the potential burden of an at-fault accident.

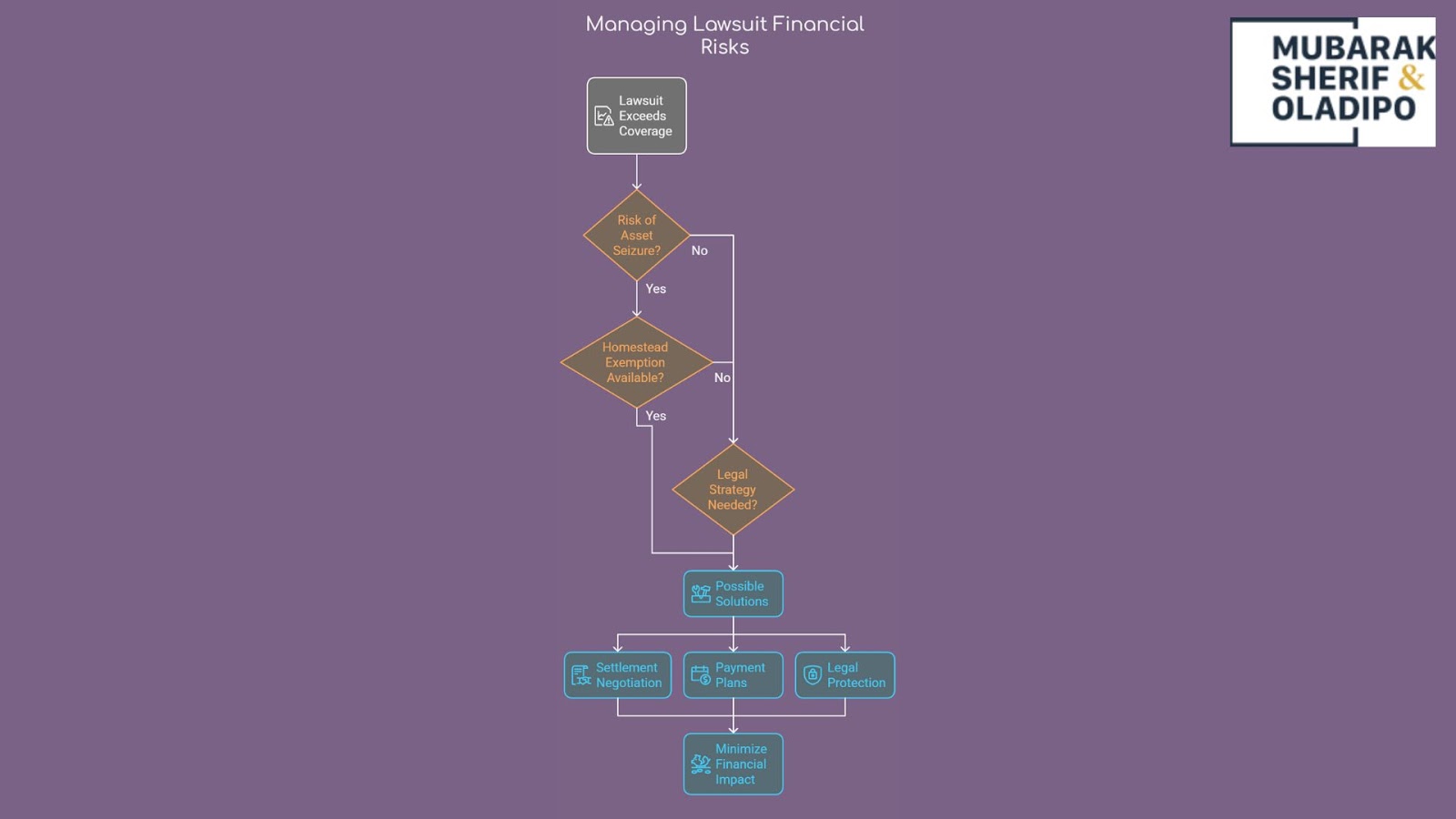

What Happens If The Lawsuit Exceeds Your Insurance Coverage?

If a lawsuit surpasses your insurance coverage, your personal assets, including your home, could be at risk. Here’s how to protect yourself financially:

- Negotiate a Settlement

- Many cases reach settlements through negotiation, often leading to manageable payment terms instead of asset loss.

- Explore Legal Options

- Payment plans and bankruptcy can provide relief, allowing individuals to restructure debt and protect essential assets.

Protect Your Home With MSO

At Mubarak, Sherif & Oladipo, PLLC, we bring a unique advantage to asset protection and personal injury law. With former insurance defense lawyers on our team, we understand the strategies insurance companies use and we use that knowledge to fight for you.

Arming yourself with the right legal strategies and professional counsel is the key to preserving your financial future and finding peace of mind amid potential liability risks. Contact us today to protect what matters most!